Digital Asset Volume Forecast Technicals (February 2025)

This section provides an in-depth breakdown of the data pipeline and statistical models used in the main report.

Data Collection & Sources

Dune Analytics retrieves and indexes real-time public blockchain data, which can be fetched on-demand with SQL queries.

I set a constraint to begin at January 1, 2021, and end at February 1, 2025, throughout the main report.

Data Collection and Preprocessing

On Dune Analytics, using SQL queries, I gathered 4 years and 1 month's worth of daily NFT and DEX volume, from January 2021 - January 2025 (inclusive), or 1492 rows of data. Then, I created an API endpoint using an API key and my query IDs on Dune to create a .csv of the query result in order to begin creating my volume forecasts.

SELECT

date_trunc('day', block_date) AS day,

SUM(amount_usd) AS total_volume

FROM

nft.trades

WHERE block_time >= TIMESTAMP '2021-01-01' AND block_time < TIMESTAMP '2025-02-01'

GROUP BY

date_trunc('day', block_date)

ORDER BY

day ASC;Then, in Python, I log transformed the data, applied some feature engineering (volatility, lag, moving average) along with holiday flags and day-of-week flags to catch cyclical patterns, and scaled everything together using RobustScaler.

import pandas as pd

import numpy as np

from sklearn.preprocessing import RobustScaler

import joblib

# load the dataset

df = pd.read_csv("nft_volume_data.csv")

# rename columns and convert date to datetime

df.rename(columns={'day': 'date', 'total_volume': 'volume'}, inplace=True)

df['date'] = pd.to_datetime(df['date'])

df = df.sort_values("date")

# apply log transformation to stabilize variance

df['volume'] = np.log1p(df['volume'])

# add a short-term moving average (3-day) to smooth noise

df['volume_ma3'] = df['volume'].rolling(window=3).mean()

# compute daily difference and 7-day volatility

df['volume_diff'] = df['volume'].diff()

df['volatility'] = df['volume'].rolling(window=7).std()

# add lag features to capture short-term dependencies

df['lag1'] = df['volume'].shift(1)

df['lag2'] = df['volume'].shift(2)

df['lag3'] = df['volume'].shift(3)

df['lag7'] = df['volume'].shift(7)

# encode day of week as sine and cosine (to capture cyclical patterns)

df['day_of_week'] = df['date'].dt.dayofweek

df['sin_day'] = np.sin(2 * np.pi * df['day_of_week'] / 7)

df['cos_day'] = np.cos(2 * np.pi * df['day_of_week'] / 7)

# is holiday flag

holiday_list = [

'2021-01-01','2021-12-25','2022-01-01','2022-12-25',

'2023-01-01','2023-12-25','2024-01-01','2024-12-25','2025-01-01'

]

holiday_dates = set(pd.to_datetime(holiday_list).date)

df['is_holiday'] = df['date'].dt.date.apply(lambda d: 1 if d in holiday_dates else 0)

# drop rows with nan values (from rolling and lag computations)

df = df.dropna()

# define parameters for sequence creation

look_back = 120 # use past 120 days as input

n_future = 30 # forecast the next 30 days

# define feature columns

features = [

'volume',

'volume_ma3',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3',

'lag7'

]

# scale all features together using robustscaler to reduce the impact of outliers

scaler = RobustScaler()

data_scaled = scaler.fit_transform(df[features].values)

joblib.dump(scaler, "scaler.pkl")

# function to create sequences for multi-step forecasting

def create_sequences(data, look_back, n_future):

X, y = [], []

for i in range(len(data) - look_back - n_future + 1):

X.append(data[i:i + look_back])

# we predict the 'volume' (index 0) for the next n_future days

y.append(data[i + look_back: i + look_back + n_future, 0])

return np.array(X), np.array(y)

X, y = create_sequences(data_scaled, look_back, n_future)

np.save("X.npy", X)

np.save("y.npy", y)

# save the preprocessed dataset for reference

df.to_csv("nft_volume_preprocessed.csv", index=False)

print("data preprocessing complete.")LSTM

Unlike standard neural networks, LSTMs have memory cells that help them remember long-term dependencies in time series data. For NFTs, I used a bidirectional LSTM model with Adam optimizer and Huber loss.

import numpy as np

import pandas as pd

import joblib

import tensorflow as tf

from tensorflow.keras.models import Sequential

from tensorflow.keras.layers import LSTM, Dense, Dropout, Bidirectional, BatchNormalization

from tensorflow.keras.regularizers import l2

from tensorflow.keras.optimizers import Adam

from tensorflow.keras.losses import Huber

from tensorflow.keras.callbacks import EarlyStopping, ReduceLROnPlateau

import matplotlib.pyplot as plt

# load the preprocessed data and sequences

df = pd.read_csv("nft_volume_preprocessed.csv")

X = np.load("X.npy")

y = np.load("y.npy")

# perform a time-based split

split_idx = int(len(X) * 0.8)

X_train, X_test = X[:split_idx], X[split_idx:]

y_train, y_test = y[:split_idx], y[split_idx:]

look_back = 120

n_future = 30

n_features = X.shape[2]

model = Sequential()

# first bidirectional lstm layer

model.add(Bidirectional(

LSTM(32, return_sequences=True, kernel_regularizer=l2(0.005)),

input_shape=(look_back, n_features)

))

model.add(Dropout(0.6))

model.add(BatchNormalization())

# second bidirectional lstm layer

model.add(Bidirectional(

LSTM(16, return_sequences=False, kernel_regularizer=l2(0.005))

))

model.add(Dropout(0.6))

model.add(BatchNormalization())

# output dense layer for forecasting n_future days

model.add(Dense(n_future, activation='linear'))

# compile the model with adam optimizer and huber loss

model.compile(optimizer=Adam(learning_rate=0.0001), loss=Huber(delta=1.0))

# set up callbacks for early stopping and reducing lr on plateau

early_stop = EarlyStopping(monitor='val_loss', patience=5, restore_best_weights=True)

reduce_lr = ReduceLROnPlateau(monitor='val_loss', factor=0.5, patience=3, min_lr=1e-6)

# train the model with callbacks

history = model.fit(

X_train, y_train,

epochs=50,

batch_size=16,

validation_data=(X_test, y_test),

callbacks=[early_stop, reduce_lr],

verbose=1

)

# save the model

model.save("lstm_nft_model_seq2seq.h5")

# plot training vs validation loss

plt.figure(figsize=(8, 5))

plt.plot(history.history['loss'], label="training loss")

plt.plot(history.history['val_loss'], label="validation loss")

plt.xlabel("epochs")

plt.ylabel("loss")

plt.legend()

plt.title("Training vs Validation Loss")

plt.show()

print("training complete and model saved.")

After training the data, I evaluated the model by comparing training versus validation loss to detect overfitting. Here, I found that both training and validation loss are decreasing and with an acceptable, decreasing gap.

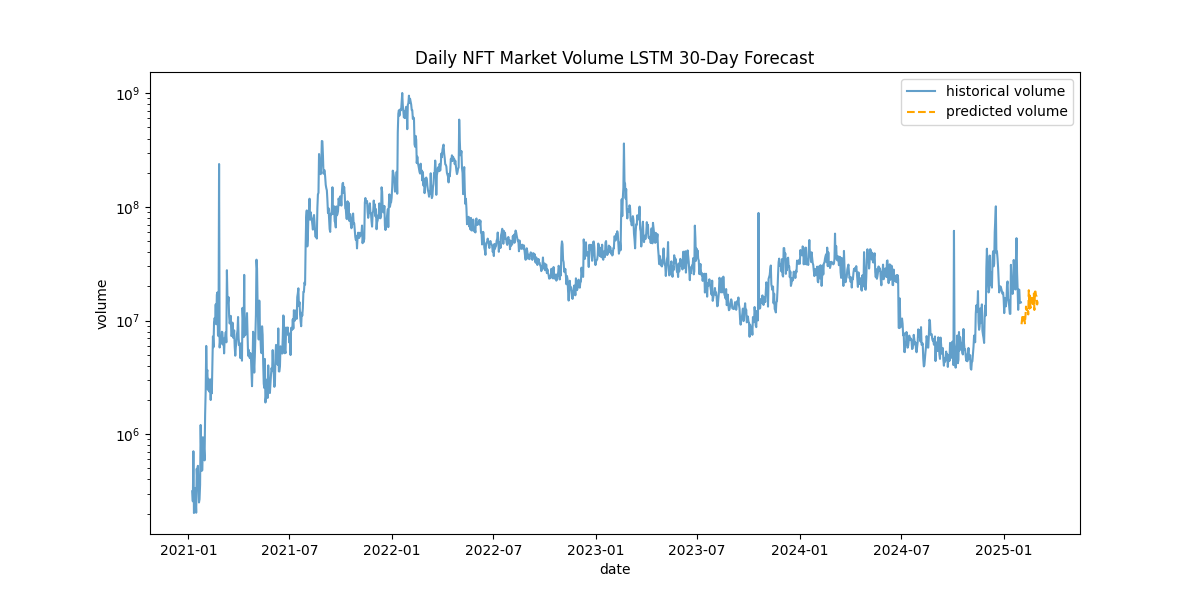

From here, I prepared input data by transforming the dataset using the scaler and extracting the last 120 days as input for the model, and then ran the prediction for the next 30 days in log-form. Then, the predictions were inverted out of log and I created a dataframe to store the predicted volume values.

import numpy as np

import pandas as pd

import joblib

import tensorflow as tf

import matplotlib.pyplot as plt

# load the trained model and scaler

model = tf.keras.models.load_model("lstm_nft_model_seq2seq.h5")

scaler = joblib.load("scaler.pkl")

# load and prepare the preprocessed dataset

df = pd.read_csv("nft_volume_preprocessed.csv")

df['date'] = pd.to_datetime(df['date'])

look_back = 120

n_future = 30

features = [

'volume',

'volume_ma3',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3',

'lag7'

]

# scale features using the saved scaler

data_scaled = scaler.transform(df[features].values)

# prepare the input sequence using the last look_back days

input_seq = data_scaled[-look_back:].reshape(1, look_back, len(features))

# predict the next n_future days (predictions are in the log-transformed domain)

predicted_log = model.predict(input_seq, verbose=0).flatten()

# function to invert scaling and reverse the log transformation

def invert_transform(values, scaler, features, index=0):

dummy = np.zeros((len(values), len(features)))

dummy[:, index] = values

inv = scaler.inverse_transform(dummy)[:, index]

return np.expm1(inv)

# get predictions on the original volume scale

predicted = invert_transform(predicted_log, scaler, features, index=0)

# create a dataframe for predicted future dates and volumes

last_date = df['date'].iloc[-1]

future_dates = pd.date_range(last_date + pd.Timedelta(days=1), periods=n_future)

pred_df = pd.DataFrame({

'date': future_dates,

'predicted_volume': predicted

})

# plot historical and predicted volumes (applying inverse log transform on historical data)

plt.figure(figsize=(12,6))

plt.plot(df['date'], np.expm1(df['volume']), label="historical volume", alpha=0.7)

plt.plot(pred_df['date'], pred_df['predicted_volume'], label="predicted volume", linestyle='dashed', color="orange")

plt.yscale("log")

plt.xlabel("date")

plt.ylabel("volume")

plt.title("Daily NFT Market Volume LSTM 30-Day Forecast")

plt.legend()

plt.show()

To confirm the model's accuracy, I built a test model for evaluation. I loaded the trained model, scaler, and dataset, created a test set from the last 150 days, extracted the last 120 days as input, and also extracted the next 30 days of actual volume to compare against predictions. I then made predictions, inverted scaling, and calculated MAE, RMSE, and MAPE.

import numpy as np

import pandas as pd

import joblib

import tensorflow as tf

from sklearn.metrics import mean_absolute_error, mean_squared_error

# load the trained model and scaler

model = tf.keras.models.load_model("lstm_nft_model_seq2seq.h5")

scaler = joblib.load("scaler.pkl")

# load and prepare the preprocessed dataset

df = pd.read_csv("nft_volume_preprocessed.csv")

df['date'] = pd.to_datetime(df['date'])

features = [

'volume',

'volume_ma3',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3',

'lag7'

]

look_back = 120

n_future = 30

# create a pseudo-test set from the last (look_back + n_future) days of historical data

test_data = df.iloc[-(look_back + n_future):].copy()

data_scaled = scaler.transform(test_data[features].values)

# prepare the input sequence from the test set (first look_back days)

input_seq = data_scaled[:look_back].reshape(1, look_back, len(features))

# actual future values (in log domain) for the next n_future days from the test set

actual_log = data_scaled[look_back:look_back + n_future, 0] # 'volume' is index 0

# model prediction for the test period

predicted_log = model.predict(input_seq, verbose=0).flatten()

# invert transformations to get original scale

def invert_transform(values, scaler, features, index=0):

dummy = np.zeros((len(values), len(features)))

dummy[:, index] = values

inv = scaler.inverse_transform(dummy)[:, index]

return np.expm1(inv)

predicted = invert_transform(predicted_log, scaler, features, index=0)

actual = invert_transform(actual_log, scaler, features, index=0)

# calculate error metrics

mae_val = mean_absolute_error(actual, predicted)

rmse_val = np.sqrt(mean_squared_error(actual, predicted))

mape_val = np.mean(np.abs((actual - predicted) / actual)) * 100

print("evaluation on historical test period:")

print(f"mae: {mae_val:.2f}")

print(f"rmse: {rmse_val:.2f}")

print(f"mape: {mape_val:.2f}%")Performance metrics on NFT data:

- MAE: 5,859,829.60

- MSE: 8,469,173.92

- MAPE: 28.79%

The MAPE, or Mean Absolute Percentage Error, expresses error as a percentage of actual values. 28.79% MAPE is acceptable, considering the inherent noisy data of the NFT market.

XGBoost

With the data already fetched and preprocessed, training using different models is made easier. I loaded the preprocessed DEX dataset, applied the scaler, created sequences using a sliding window, flattened the data for XGBoost, used MultiOutputRegressor to handle multi-step forecasting (since XGBoost doesn't do that inherently), computed model evaluation metrics (MAE, RMSE, and MAPE) on the test set for performance assessment, and forecasted the next 30 days of DEX market volume:

import numpy as np

import pandas as pd

import joblib

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

from sklearn.multioutput import MultiOutputRegressor

from xgboost import XGBRegressor

from sklearn.metrics import mean_absolute_error, mean_squared_error

# load preprocessed data

df = pd.read_csv("dex_volume_preprocessed.csv")

df['date'] = pd.to_datetime(df['date'])

# define feature list

features = [

'volume',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3'

]

# define parameters

look_back = 120 # number of past days used as input

n_future = 30 # number of days to forecast

# load the pre-fitted scaler and scale data

scaler = joblib.load("scaler.pkl")

data_scaled = scaler.transform(df[features].values)

# create sequences using a sliding window

def create_sequences(data, look_back, n_future):

X, y = [], []

for i in range(len(data) - look_back - n_future + 1):

X.append(data[i:i + look_back])

# predict the 'volume' feature (index 0) for the next n_future days

y.append(data[i + look_back: i + look_back + n_future, 0])

return np.array(X), np.array(y)

X_seq, y_seq = create_sequences(data_scaled, look_back, n_future)

# xgboost expects 2d tabular data, so flatten the time dimension

n_samples = X_seq.shape[0]

X_flat = X_seq.reshape(n_samples, -1) # shape becomes (n_samples, look_back * number_of_features)

# split data into training and testing sets (no shuffling, to preserve time order)

X_train, X_test, y_train, y_test = train_test_split(X_flat, y_seq, test_size=0.2, shuffle=False)

# build and train the xgboost model using multioutputregressor for multi-step forecasting

xgb_model = MultiOutputRegressor(

XGBRegressor(

objective='reg:squarederror',

n_estimators=100,

learning_rate=0.1,

max_depth=5,

random_state=42

)

)

xgb_model.fit(X_train, y_train)

# evaluate the model on the test set

y_pred = xgb_model.predict(X_test)

mae_val = mean_absolute_error(y_test, y_pred)

rmse_val = np.sqrt(mean_squared_error(y_test, y_pred))

mape_val = np.mean(np.abs((y_test - y_pred) / y_test)) * 100

print("xgboost model evaluation on test set:")

print(f"mae: {mae_val:.2f}")

print(f"rmse: {rmse_val:.2f}")

print(f"mape: {mape_val:.2f}%")

# forecast the next 30 days using the most recent data

last_input = data_scaled[-look_back:].reshape(1, -1)

xgb_forecast_log = xgb_model.predict(last_input).flatten()

# function to invert scaling and reverse the log transformation

def invert_transform(values, scaler, features, index=0):

dummy = np.zeros((len(values), len(features)))

dummy[:, index] = values

inv = scaler.inverse_transform(dummy)[:, index]

return np.expm1(inv)

# invert transformation for the forecast

xgb_forecast = invert_transform(xgb_forecast_log, scaler, features, index=0)

# visualization

plt.figure(figsize=(12, 6))

plt.plot(df['date'], np.expm1(df['volume']), label="historical volume", alpha=0.7)

last_date = df['date'].iloc[-1]

future_dates = pd.date_range(last_date + pd.Timedelta(days=1), periods=n_future)

plt.plot(future_dates, xgb_forecast, label="xgboost forecast", linestyle='dashed', color="orange")

plt.yscale("log")

plt.xlabel("date")

plt.ylabel("volume")

plt.title("Daily DEX Market Volume XGBoost 30-Day Forecast")

plt.legend()

plt.show()

Performance metrics on DEX data:

- MAE: 0.08

- RMSE: 0.10

- MAPE: 13.49%

Hybrid

I also built a hybrid model in an attempt to take advantage of each of their strengths, with LSTMs being great at capturing temporal dependencies and sequential patterns and XGBoost excelling at handling non-linear relationships and dealing with noise in data to capture complex patterns. I trained a linear regression metamodel to combine their predictions, then forecasted the next 30 days using the hybrid model. For DEX:

import numpy as np

import pandas as pd

import joblib

import tensorflow as tf

from sklearn.multioutput import MultiOutputRegressor

from xgboost import XGBRegressor

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_absolute_error, mean_squared_error

import matplotlib.pyplot as plt

# load preprocessed data

df = pd.read_csv("dex_volume_preprocessed.csv")

df['date'] = pd.to_datetime(df['date'])

# define feature list

features = [

'volume',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3'

]

# define parameters

look_back = 120 # number of past days used as input

n_future = 30 # number of days to forecast

# load the pre-fitted scaler and scale the data

scaler = joblib.load("scaler.pkl")

data_scaled = scaler.transform(df[features].values)

# function to create sequences for multistep forecasting

def create_sequences(data, look_back, n_future):

X, y = [], []

for i in range(len(data) - look_back - n_future + 1):

X.append(data[i : i + look_back])

# predict the 'volume' feature (index 0) for the next n_future days

y.append(data[i + look_back : i + look_back + n_future, 0])

return np.array(X), np.array(y)

# create sequences from the scaled data

X_seq, y_seq = create_sequences(data_scaled, look_back, n_future)

# for hybrid metamodel training, select the last 100 sequences

meta_samples = 100 if X_seq.shape[0] >= 100 else X_seq.shape[0]

meta_X = X_seq[-meta_samples:]

meta_y = y_seq[-meta_samples:]

# load the pre-trained lstm model

lstm_model = tf.keras.models.load_model("lstm_dex_model_seq2seq.h5")

# get lstm predictions

lstm_preds = []

for i in range(meta_X.shape[0]):

pred = lstm_model.predict(meta_X[i : i + 1], verbose=0).flatten()

lstm_preds.append(pred)

lstm_preds = np.array(lstm_preds) # shape (meta_samples, n_future)

# prepare xgboost by flattening the time dimension

meta_X_flat = meta_X.reshape(meta_X.shape[0], -1)

# build and train the xgboost model

n_samples = X_seq.shape[0]

X_flat = X_seq.reshape(n_samples, -1)

xgb_model = MultiOutputRegressor(

XGBRegressor(

objective='reg:squarederror',

n_estimators=100,

learning_rate=0.1,

max_depth=5,

random_state=42

)

)

xgb_model.fit(X_flat, y_seq)

# get xgboost predictions

xgb_preds = xgb_model.predict(meta_X_flat)

# combine predictions from lstm and xgboost

meta_features = np.hstack([lstm_preds, xgb_preds])

meta_targets = meta_y

# train a linear regression metamodel (using multioutputregressor) to combine base model predictions

meta_model = MultiOutputRegressor(LinearRegression())

meta_model.fit(meta_features, meta_targets)

# forecast

last_seq = data_scaled[-look_back:].reshape(1, look_back, len(features))

lstm_forecast = lstm_model.predict(last_seq, verbose=0).flatten() # shape (n_future,)

last_seq_flat = data_scaled[-look_back:].reshape(1, -1)

xgb_forecast = xgb_model.predict(last_seq_flat).flatten() # shape (n_future,)

hybrid_features = np.hstack([lstm_forecast, xgb_forecast]).reshape(1, -1)

hybrid_forecast_log = meta_model.predict(hybrid_features).flatten()

# invert scaling and reverse the log transformation

def invert_transform(values, scaler, features, index=0):

dummy = np.zeros((len(values), len(features)))

dummy[:, index] = values

inv = scaler.inverse_transform(dummy)[:, index]

return np.expm1(inv)

# invert transformation for the hybrid forecast

hybrid_forecast = invert_transform(hybrid_forecast_log, scaler, features, index=0)

# visualization

plt.figure(figsize=(12, 6))

plt.plot(df['date'], np.expm1(df['volume']), label="historical volume", alpha=0.7)

last_date = df['date'].iloc[-1]

future_dates = pd.date_range(last_date + pd.Timedelta(days=1), periods=n_future)

plt.plot(future_dates, hybrid_forecast, label="hybrid forecast", linestyle='dashed', color="green")

plt.yscale("log")

plt.xlabel("date")

plt.ylabel("volume")

plt.title("Daily DEX Market Volume LSTM + XGBoost 30-Day Forecast")

plt.legend()

plt.show()

To assess the model's accuracy, I built a script to train the model on a test set and calculated performance metrics (MAE, RMSE, MAPE) and plotted the forecast vs actual to get a sense of how the model performs versus reality.

import numpy as np

import pandas as pd

import joblib

import tensorflow as tf

from sklearn.model_selection import train_test_split

from xgboost import XGBRegressor

from sklearn.multioutput import MultiOutputRegressor

from sklearn.linear_model import LinearRegression

from sklearn.metrics import mean_absolute_error, mean_squared_error

import matplotlib.pyplot as plt

# load preprocessed data

df = pd.read_csv("dex_volume_preprocessed.csv")

df['date'] = pd.to_datetime(df['date'])

# define feature list

features = [

'volume',

'volume_diff',

'volatility',

'sin_day',

'cos_day',

'is_holiday',

'lag1',

'lag2',

'lag3'

]

# define parameters

look_back = 120 # number of past days used as input

n_future = 30 # number of days to forecast

# load the scaler and scale the data

scaler = joblib.load("scaler.pkl")

data_scaled = scaler.transform(df[features].values)

# function to create sequences for multistep forecasting

def create_sequences(data, look_back, n_future):

X, y = [], []

for i in range(len(data) - look_back - n_future + 1):

X.append(data[i:i + look_back])

# predict the 'volume' feature (index 0) for the next n_future days

y.append(data[i + look_back: i + look_back + n_future, 0])

return np.array(X), np.array(y)

# create sequences from the scaled data

X_seq, y_seq = create_sequences(data_scaled, look_back, n_future)

# split data into training and test sets (preserving time order)

X_train, X_test, y_train, y_test = train_test_split(X_seq, y_seq, test_size=0.2, shuffle=False)

# flatten the time dimension

n_samples_train = X_train.shape[0]

X_train_flat = X_train.reshape(n_samples_train, -1)

# train xgboost model on training set

xgb_model = MultiOutputRegressor(

XGBRegressor(

objective='reg:squarederror',

n_estimators=100,

learning_rate=0.1,

max_depth=5,

random_state=42

)

)

xgb_model.fit(X_train_flat, y_train)

# load the pre-trained lstm model

lstm_model = tf.keras.models.load_model("lstm_dex_model_seq2seq.h5")

# create meta training data from the last part of the training set

meta_train_size = min(100, X_train.shape[0])

meta_X_train = X_train[-meta_train_size:]

meta_y_train = y_train[-meta_train_size:]

# get base model predictions (lstm and xgboost) on meta training samples

lstm_meta_preds = []

xgb_meta_preds = []

for i in range(meta_train_size):

sample = meta_X_train[i:i+1]

# get lstm prediction

pred_lstm = lstm_model.predict(sample, verbose=0).flatten()

lstm_meta_preds.append(pred_lstm)

# flatten sample for xgboost input

sample_flat = sample.reshape(1, -1)

pred_xgb = xgb_model.predict(sample_flat).flatten()

xgb_meta_preds.append(pred_xgb)

lstm_meta_preds = np.array(lstm_meta_preds)

xgb_meta_preds = np.array(xgb_meta_preds)

# combine base model predictions to form meta features

meta_features_train = np.hstack([lstm_meta_preds, xgb_meta_preds])

# train a linear regression metamodel (wrapped in multioutputregressor) to combine predictions

meta_model = MultiOutputRegressor(LinearRegression())

meta_model.fit(meta_features_train, meta_y_train)

# evaluate the hybrid model on the test set

n_samples_test = X_test.shape[0]

lstm_test_preds = []

xgb_test_preds = []

for i in range(n_samples_test):

sample = X_test[i:i+1]

pred_lstm = lstm_model.predict(sample, verbose=0).flatten()

lstm_test_preds.append(pred_lstm)

sample_flat = sample.reshape(1, -1)

pred_xgb = xgb_model.predict(sample_flat).flatten()

xgb_test_preds.append(pred_xgb)

lstm_test_preds = np.array(lstm_test_preds)

xgb_test_preds = np.array(xgb_test_preds)

meta_features_test = np.hstack([lstm_test_preds, xgb_test_preds])

# use metamodel to generate hybrid predictions on test set

hybrid_test_preds = meta_model.predict(meta_features_test)

# calculate evaluation metrics on test set for hybrid model

mae_val = mean_absolute_error(y_test, hybrid_test_preds)

rmse_val = np.sqrt(mean_squared_error(y_test, hybrid_test_preds))

mape_val = np.mean(np.abs((y_test - hybrid_test_preds) / y_test)) * 100

print("hybrid model evaluation on test set:")

print(f"mae: {mae_val:.2f}")

print(f"rmse: {rmse_val:.2f}")

print(f"mape: {mape_val:.2f}%")

# visualization

plt.figure(figsize=(12,6))

plt.plot(y_test[0], label="actual forecast")

plt.plot(hybrid_test_preds[0], label="hybrid forecast", linestyle='dashed', color="green")

plt.xlabel("day")

plt.ylabel("scaled volume")

plt.title("LSTM + XGBoost Model Forecast vs Actual (Test Sample)")

plt.legend()

plt.show()Performance metrics on DEX data:

- MAE: 0.10

- RMSE: 0.12

- MAPE: 18.28%

Model Limitations

This study assumes a stationary relationship between DEX and NFT markets, but in reality market structures change and evolve over time. For example, NFTs experienced a mania in 2021 that made data prior to that practically irrelevant.